Event Contracts

How Polymarket and Kalshi Slip Through the Red Tape

Mainsail Fund Update- Since opening the doors in April the fund is +18.42%. Even better: a Sharpe of 2.26 and a 0.06 correlation to the S&P (SPY). In plain English, that Sharpe means we’re delivering very strong risk-adjusted returns (roughly 2.26 units of excess return per unit of volatility) — and the near-zero correlation means our performance is essentially independent of broad market moves.

If you want a quick litmus test for your advisor: ask them for their Sharpe and correlation over the same period. If they don’t have numbers that look anything like this, you might have an awkward but useful conversation at dinner.

One thought experiment to chew on: avoiding the big drawdowns since 2000 would have turned many portfolios into something wildly larger (some estimates cite figures like +100%). Let that sink in — downside control compounds just as dramatically as upside.

Questions about the fund or the numbers? Hit me up. I’ll happily walk you through my methodology, risk management, and how we generate alpha.

“Losers assemble in small groups and complain, winners assemble as a team and find ways to win.” — Bill Parcells.

Jets fans, let’s be honest—did you really expect anything different this season? For 14 years I was that delusional diehard, chanting “this is our year” like a broken record. But after the heartbreak of 2024’s overhyped collapse, I’ve downgraded myself to a casual observer—much to my kids’ disappointment. Want to earn me back as a fan? Simple: just make the playoffs. It’s only been, oh, 15 years. Rant over—now onto the good stuff.

Since we’re already in the betting mood with event contracts, here’s one for the weekend slate: take the Bucs to cover against the Jets. New York’s defense couldn’t stop a nosebleed right now, and with a second-string QB under center in Tampa, this one looks lopsided.

What I was watching and reading this week

I wrapped up Inner Excellence last week and dove straight into Burn Book by Kara Swisher. It’s part memoir, part Silicon Valley exposé, tracing her rise from sharp-edged reporter to insider-critic over three decades. Along the way, she dishes on candid encounters with tech’s biggest names, celebrates the early spirit of innovation, and doesn’t hold back on how power, greed, and a lack of accountability corroded those ideals. Layered in is her own journey—the choices, the costs, and her still-stubborn belief that tech, for all its darker turns, can be a force for good. Now, shifting from books to markets, let’s dig into this past week’s data…

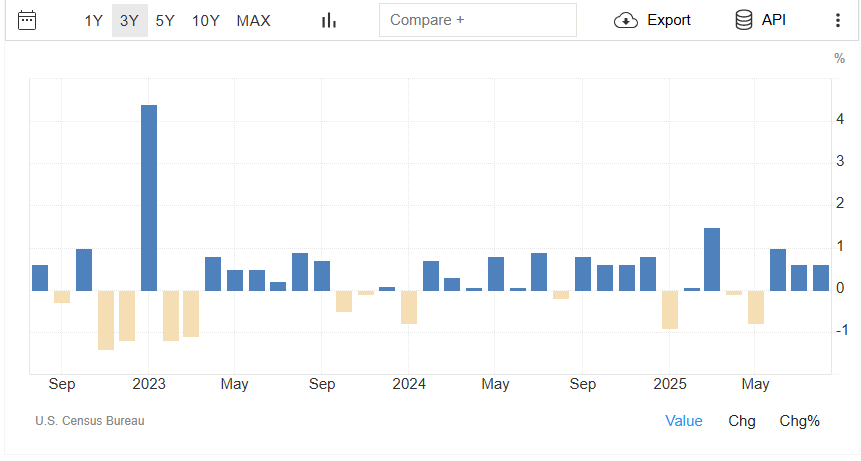

Retail Sales- U.S. retail sales came in stronger than expected, with August sales rising 0.6% month-over-month versus July and climbing about 5% from a year earlier. Core retail sales, which strip out autos, gasoline, building materials, and food services, advanced 0.7%—a solid beat against forecasts of just 0.2%. Online and non-store retailers were standouts, posting more than 10% year-over-year growth, while restaurants and bars gained around 6.5%. The upside surprise suggests that consumer demand remains resilient despite signs of a softening labor market, though part of the growth may reflect higher prices from inflation and tariffs rather than pure volume gains. The report reinforces the idea that consumer spending continues to underpin the economy, which could temper expectations for aggressive Fed rate cuts, while providing a modest tailwind for equities tied to discretionary and e-commerce sectors.

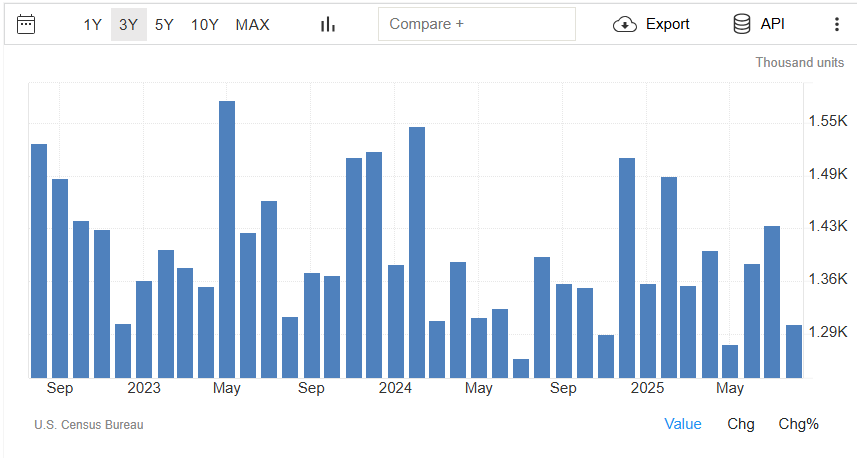

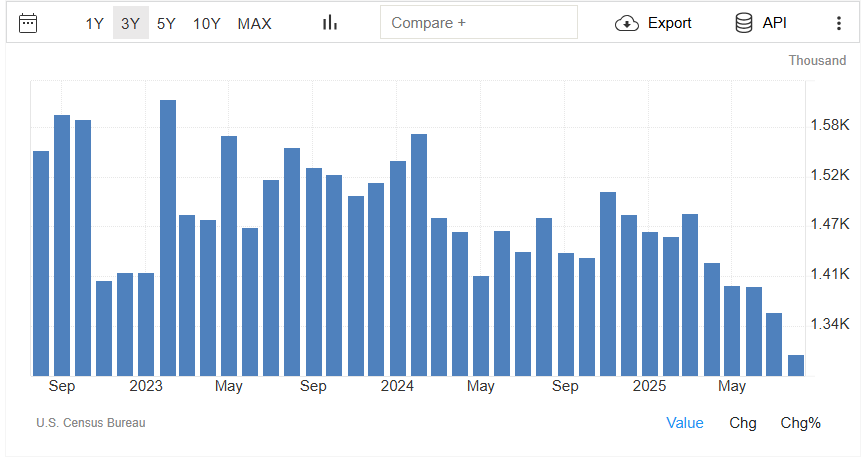

Housing Starts

Building Permits

Housing Starts/Building Permits- both took a step back in August, signaling a cooling pipeline for residential construction. Permits for new homes slipped to about 1.31 million units annualized, down from July and more than 11% below last year, while housing starts fell to 1.31 million units, a sharp decline from the prior month. Single-family activity was hit particularly hard, with both permits and starts moving lower. At the same time, completions ticked up, adding to supply already in the pipeline. The picture that emerges is one of cautious builders—finishing what’s underway but hesitating on new projects amid elevated mortgage rates, softer demand, and persistent labor and cost pressures. If rates continue to ease into year-end, we could see permits rebound, but for now the data suggest a more measured pace of building ahead.

FOMC Decision- The Fed’s recent 25bp cut, coupled with clear guidance for two more, fits squarely into a well-worn historical pattern of non-recession easing cycles. Since 1980, three such episodes (1995, 1998, and 2019) have delivered strong near-term equity gains, with the S&P 500 typically rallying in the first 1–3 months as markets priced in further cuts. The most relevant parallel is 1995, when a soft landing followed prior tightening, producing a +21% one-year return and more than doubling over three years. In every case, the key ingredients were present: a healthy economy, markets near all-time highs, and the Fed signaling more easing ahead. Today’s backdrop—4.3% unemployment, steady growth, and indexes pressing highs—mirrors those conditions. While risks remain from inflation or weakening data, history argues strongly for continued equity strength over the coming months, with this cycle shaping up most like the 1995 playbook. At some point, this cycle runs out of buyers. Are we sitting in 1998, 1999, or the early stages of 2000? I can’t say with certainty—but if the signals or data shift, I’ll be sure to call it out.