Global Dollar Deficit

Adding stress to the markets

“The key to the game is your capital reserves. If you don’t have enough, you can’t piss in the tall weeds with the big dogs.”- Wall St

When it comes to managing capital, the game is won by those who survive the volatility, not those who heroically buy every dip. Dry powder and position sizing matter more than victory laps — smaller size for bigger swings, and cash set aside for the names you truly want at better prices. If you’re fully levered and reflexively adding risk into every selloff, that’s not a strategy — that’s a countdown clock to blowing up a fund.

Lately, pockets of BTC and AI speculation look like they’ve misplaced that lesson, and under the hood the market tone is getting louder and less forgiving. Nasdaq and Russell vol are creeping toward the 30-handle, which implies ~2% daily swings at the index level and 5–10% moves for the higher-beta names.

As we head into a headline-loaded stretch — with the SCOTUS tariff ruling and a heavy slate of economic data acting as potential macro tripwires — there are a few clean signals to watch to determine whether we break lower or reset into risk-on mode. The checklist: Mag-7 leadership, Fed liquidity posture, and the VIX. If GOOGL, AMZN, AAPL, and NVDA can stabilize and push higher, that opens the door for investors to re-engage on the long side. But for that to stick, we’ll likely need the VIX to break back below 20 and actually live there, not just dip intraday.

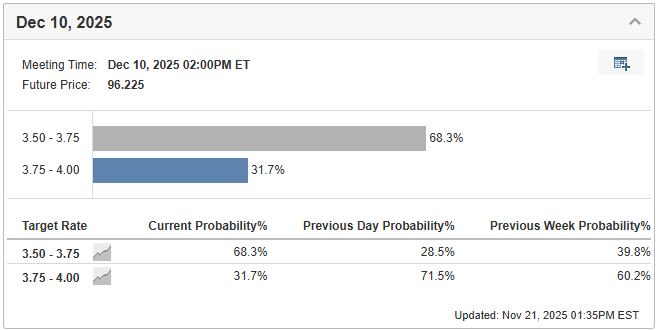

Meanwhile, the market is back to pricing a –25 bps cut for December, a shift from the “no-cut” stance we were sitting at just a few days ago.

If conditions continue drifting toward risk-off into year-end, I’ll flag it in next week’s note — there’s no need to panic or start declaring the AI supercycle dead on arrival. I’ve heard plenty of bubble-burst narratives making the rounds, but until credit cracks and the mega-cap leaders roll over, it’s still business as usual. The playbook doesn’t change: higher volatility means wider price swings and demands smaller position sizing. Stay liquid, stay patient, and let the tape reveal who is over levered.

What I was watching and reading this week

I just started a new book called The Man Behind the Microchip, about Bob Noyce — a small-town Midwestern kid who blended curiosity, hustle, and engineering brilliance long before Silicon Valley existed. Even as a kid he was running businesses and constantly taking things apart to understand how they worked. Later, when he discovered the transistor and ultimately helped pioneer the integrated circuit, he essentially lit the fuse that made exponential computing power possible.

We often celebrate Gates, Jobs, Dell, and other modern tech visionaries, but Noyce is the one who truly set the stage. Without him, the digital world we live in — from laptops to rockets to AI — might still be stuck in the analog age.

NVDA Earnings- Another blowout quarter — they beat on both the top and bottom line. Jensen Huang said Blackwell demand is off the charts and cloud GPUs are completely sold out. It’s exactly the kind of relief the market needed and should help steady the tech tape in the near term. But if this pop got faded quickly, that’s your signal the selling pressure isn’t done, and we may be leaning into a more risk-off tone into year-end.

There’s also no shortage of chatter about an AI bubble, especially with the chaos in crypto and some AI-adjacent names getting absolutely nuked. But bubbles rarely burst when everyone is worried — they burst when everyone is crammed on the same side of the boat. If anything, this market probably has to ramp even higher to force the bears to capitulate before any real break lower happens. When does that moment arrive? Your guess is as good as mine — but the signs aren’t there yet.

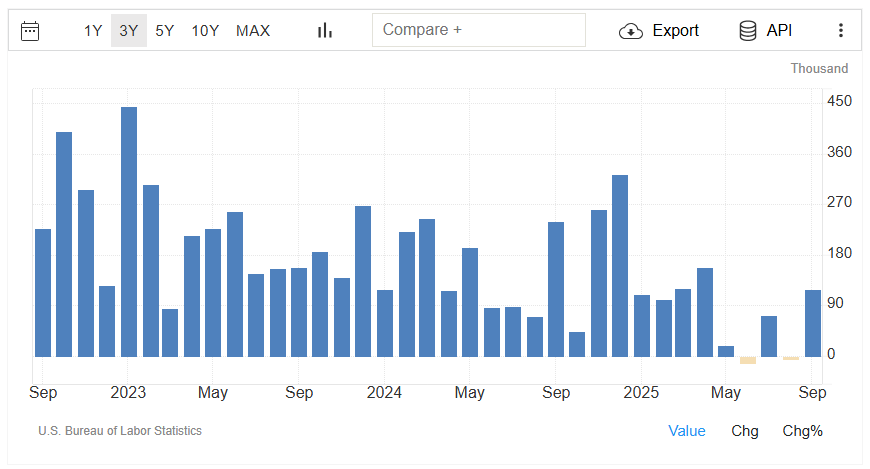

NFP number- Big surprise here, though at this point I’m not sure what to believe with half the economic data showing up weeks late. This is the September jobs report, finally landing six weeks behind schedule — 119k vs. 50k expected, so more than double the estimate. What’s odd is that bond yields actually moved lower on the release, which isn’t the reaction you’d expect from a stronger-than-forecast print. Just another reminder of how much noise there is to sift through in this market right now.

The Main Course

I asked my AI assistant this week to help translate the dollar-shortage story into plain English for those of you who aren’t glued to markets every day and prefer a cleaner, more readable breakdown. Let me know if this makes sense — I’m happy to dive deeper if anyone wants the full version.