The Narrowest Path

When four tickers carry the world: Deconstructing the semi cap-driven surge in the SPY.

The kids are out of school next week, marking the end of a semester that felt like an entire market cycle crammed into four months. We’ve seen a year’s worth of volatility since January, but the change in weather hasn't cooled the macro environment. With the Iran conflict still driving input costs higher, the squeeze on the consumer remains the dominant story. I’m stepping away from the desk from next Wednesday through June 3rd to head overseas. A fun trip planned for the family—my son is finally catching his first Premier League game and the rest of the family some tennis at Roland-Garros.

What I was reading and watching this week

I’ve started a new book this week: Wealth, War and Wisdom by the legendary Barton Biggs. Although it was published nearly two decades ago, its core thesis feels incredibly relevant in today’s environment. We are currently navigating a significant "war overhang" that is distorting asset prices across almost every sector. Biggs provides a masterclass on how geopolitical conflict reshapes markets, illustrating through history how specific nations emerged from periods of chaos either fundamentally strengthened or permanently diminished. It’s a timely reminder that while history doesn't repeat, it certainly rhymes—especially when it comes to the intersection of global conflict and capital preservation.

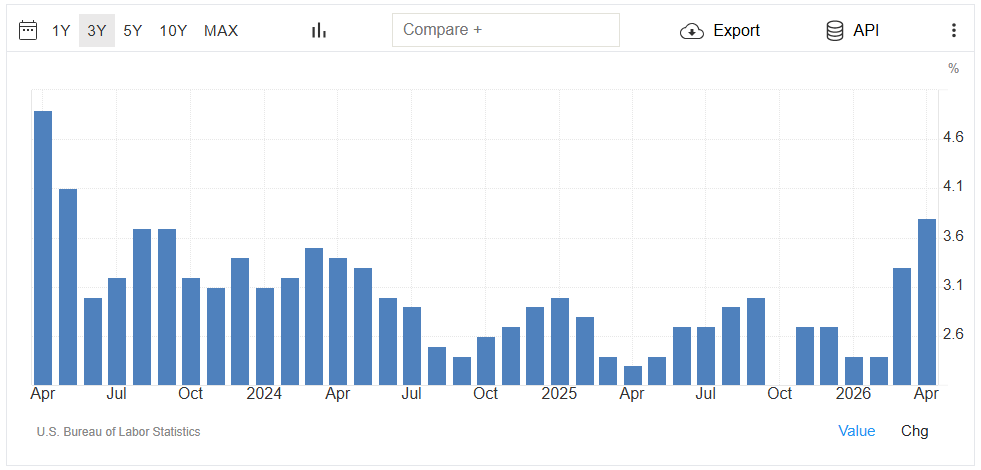

CPI- showed that annual inflation accelerated to 3.8%, up from 3.3% in March and slightly above consensus expectations of 3.7%. Monthly headline inflation rose 0.6%, driven primarily by a persistent oil shock that pushed energy costs up 17.9% year-over-year—with gasoline prices specifically jumping over 28%. Core CPI, which excludes food and energy, also ticked higher to 2.8% annually (0.4% monthly), fueled by normalization in shelter and rent data following last year's collection gaps. Overall, the "hotter than expected" print signals that inflationary pressure remains sticky, likely keeping the Federal Reserve on a cautious, "higher-for-longer" path as the market continues to price in the effects of ongoing energy volatility.

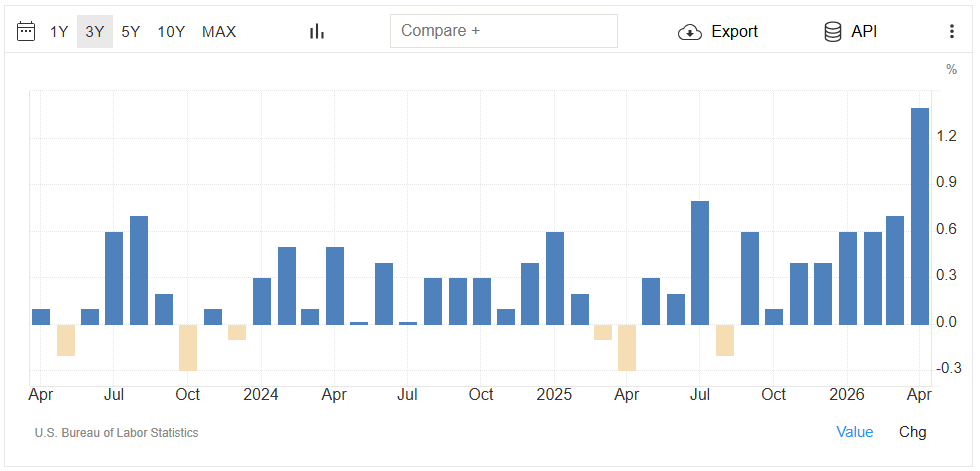

PPI- released this week (May 13) added further pressure to the "higher-for-longer" narrative. Wholesale prices jumped 0.7% for the month, significantly overshooting the 0.3% consensus estimate. The primary driver was a sharp spike in the "Goods" component, which surged 1.2%, largely reflecting the same energy-related volatility seen in the consumer data. Core PPI (excluding food and energy) also rose a firm 0.5%, suggesting that sticky input costs are beginning to work their way through the entire supply chain. For the markets, this back-to-back heat in inflation data suggests that producer margins are being squeezed by the very "real assets" (energy and materials) that you’ve been tracking, further complicating any hopes for a Federal Reserve pivot in the near term.

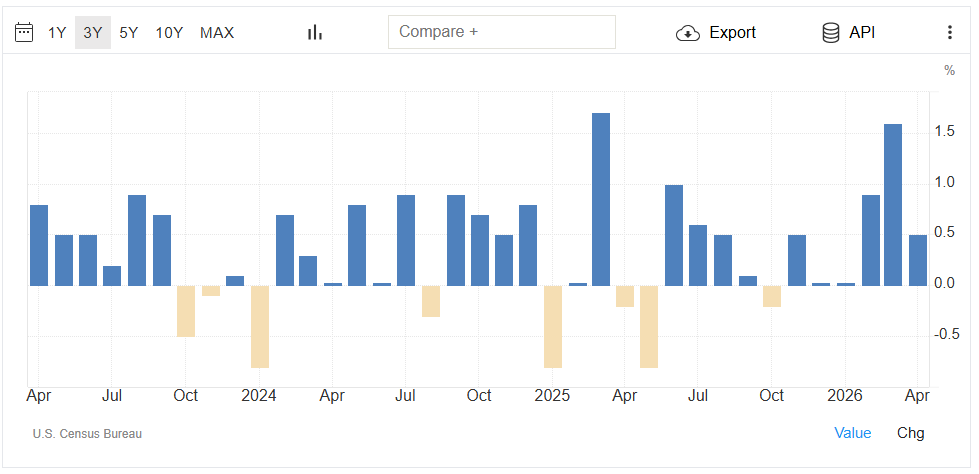

Retail Sales- report shows a consumer that is resilient but slowing under the weight of surging energy costs. Headline sales rose 0.5% month-over-month, matching expectations but decelerating significantly from March’s revised 1.6% jump. The primary driver was once again the pump, with gasoline station sales up 2.8% following the previous month's massive 13.7% spike. However, the "control group"—which filters out volatile categories like autos and gas and is used to calculate GDP—rose a solid 0.5%, beating the 0.4% forecast and suggesting that underlying demand remains durable despite the "inflation shock" from the ongoing conflict in Iran.

The Main Course

Most people would be shocked to learn that the S&P 500's upward trajectory this year is essentially a four-man show: SanDisk, Micron, Intel, and Nvidia. If you weren’t trading during the 1999–2001 boom, it’s hard to describe the atmosphere, but I remember it well. I was the college kid skipping class to chase tickers on E*Trade, riding the same wave of euphoria and FOMO currently sweeping the tape. They say history doesn't repeat, but it’s definitely rhyming right now.